Basics of the HIRO Program

The HIRO program, administered by Fannie Mae, is a loan program designed to help get homeowners a lower rate and payment options even in circumstances where they may have little or no equity in their home yet. The HIRO program is very different from most other refinancing programs, as they usually require equity in order to refinance no matter how good your income or credit rating may be.

And while the appreciation of homes has generally occurred for most areas in the nation, this appreciation isn’t uniform, and other regions are experiencing stagnant home prices or even depreciation. The rise in equity potential is very uneven, and the latest data shows that in the fourth quarter of 2019, 3.5 million US homes – one in 16 - were seriously underwater with a mortgage loan balance that is at least 25% higher than their home’s value. These borrowers are the ones that the HIRO program could advantage the most.

HIRO and LTV Ratios

The biggest advantage of the Fannie Mae High LTV Refinance option is that there is no maximum loan-to-value (LTV) for 30- and 15-year fixed-rate mortgages. This allowance ensures that even loans with high LTVs (in excess of 125% of the home’s current value) can qualify and enjoy the benefits of the program. Adjustable-rate mortgages are still eligible for HIRO refinancing, but they do have a maximum LTV value of 105% of the property’s value. ARM loans with higher LTVs would be ineligible.

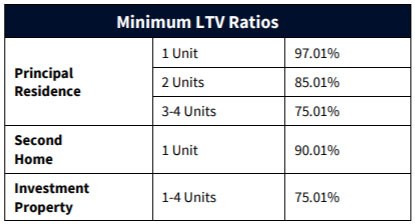

Despite having no maximum LTV, there are minimum LTVs. That means many borrowers may have too much equity to qualify for the HIRO program if they are in an area that has had rapid appreciation. For single-family homes that are primary residences, this figure is 97.01%, although Fannie Mae has published the maximum LTV values for other types of properties as well.

Provided the property being refinanced meets these minimum LTV thresholds, as well as other conditions, then the mortgage may be eligible for the program.

Benefits of the HIRO Program

The HIRO program can offer multiple benefits for potential borrowers depending upon their unique circumstances, including but not limited to:

- A reduced monthly principal and interest payment, meaning the borrower will likely pay less each month and over the life of the loan.

- A lower interest rate for the life of the loan. Today’s rates are at historic lows, making it an ideal time to refinance using HIRO.

- A shorter amortization term if you switch from a 30-year to a 15-year term allowing you to build equity faster.

- A more stable mortgage solution – such as may be experienced when an adjustable-rate mortgage is refinanced to a HIRO fixed-rate mortgage.

- Simplified financial documentation requirements.

- Transferrable mortgage insurance.

The HIRO program, as a replacement to the HARP loan program, is an excellent option for borrowers who haven’t experience home appreciation as they may have expected. Given the current, historically low-interest rates, it may be an excellent time to explore whether HIRO refinancing is an option for you.